Bank of Ceylon Financial Accounts for the year 2021 Reveals an unlawful and unethical transfer of Rs. 6,769,360,000 out of Superannuation Funds.

It is mandatory for Banks to publish their Annual Statement of accounts in full, either by a printed Report or in a web-site before the 1st of April in the following year, in terms of regulations issued by the Central Bank. The Bank of Ceylon has not, as yet (14.04.2022) conformed to this, but has uploaded the statement in the Colombo Stock Exchange web-site, due to some other requirement, as a listed company in the stock exchange. Thus, this statement is not yet known to the general public.

A team of experts consisting of retired senior executives of the People's Bank and Bank of Ceylon, who work closely with the Pahantemba Organisation, a social activist group operating in the financial sector, examined the Annual Statement of Accounts of the Bank of Ceylon, as it appears in the stock exchange web-site, has reported that the statement of accounts does not reflect a realistic fair view of the assets and liabilities of the Bank, as it depicts in many aspects, unreal and manipulated versions of the truth. The shocking discovery is the transfer of Rs. 6,769,360,000 out of the Superannuation Funds and adding the sum to the annual profit, on the spurious basis of an "actuarial gain" declared, through a fraudulent manipulation of the assumptions which base the actuarial assessment. This transfer is both unlawful and unethical. This will be reported by us to the Central Bank, the Ministry of Finance and the International Monetary Fund, all of which monitor closely, the finances of the country which is in deep waters, presently.

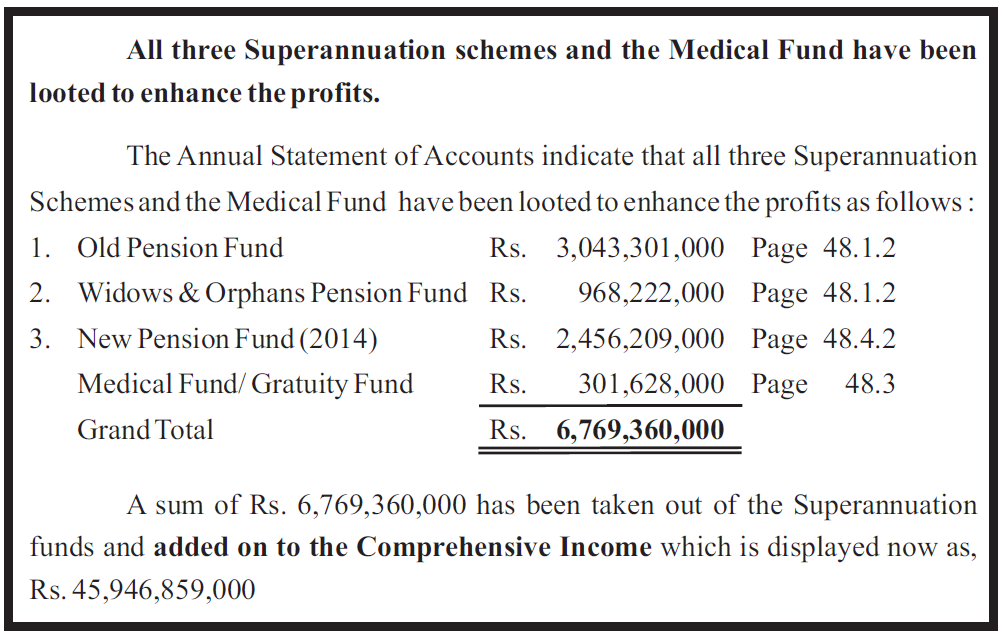

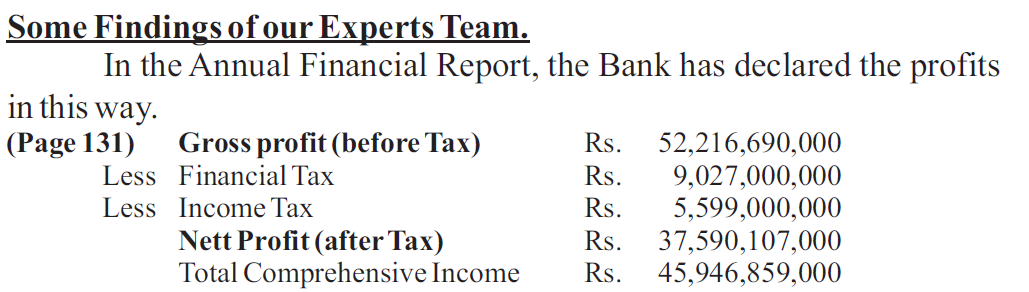

While the Bank has announced its gross profit as Rs. 52,216,690,000 and net profit as Rs. 37,590,107,000, yet, in an explanation note, pages 116, 130 & 131, it also quotes another profit figure of Rs. 45,946,859,000 by adding an amount of Rs. 8,357 billion on the basis of "other comprehensive income for the year", within which the total actuarial gain of Rs. 6,769,360,000 is also included.

This is of course, very confusing statistics for any layman, uninitiated in the art of deceptions of international audit crooks like Water House Coopers, KPMG, Ernst Young etc., The entire statement should be subjected to a forensic audit, by the International Monetary Fund. In 1992, when the IMF conducted a forensic audit of the two main commercial banks, the Bank of Ceylon and People's Bank, it declared that the two Banks were "technically Bankrupt."

This is an Asset, but consists of components which are mere book entries and never-recorerable loans, such as loans/overdrafts granted to state – owned enterprises, which are now publicly declared as bankrupt. For accounting purposes, such lending though covered by government guaranties by way of Letters of Comfort, their validity at present is null and void, due to the country rating by International Rating Agencies being fallen below "B", and is due to be listed soon as bankrupt for dishonoring sovereign bond obligations. Massive lending to Petroleum Corporation, Electricity Board, Paddy Marketing Board, Sri Lanka Airlines and Road Development Authority are consistently never recoverable but the lending continues to increase. The Overdrawn balances on the account of the Deputy Secretary to the Treasury (DST) is currently Rs. 500 billion for BOC and Rs. 350 billion for P.B. totaling Rs. 850 billion. This is unlikely to be recovered.

Thus, these facilities which are really non-performing are listed in the current portfolio, which is a distortion, tantamount to a wrongful depiction of a Liability as an Asset.

This figure includes interest to be paid by the state- owned enterprises, which are currently bankrupt. 52.3% of the lending of state – owned banks are to the S.O.E.s Therefore, "receivables" from them are mere fiction.

Non-Performing Advances (Page 368)

The old, Non-Performing Advances are now termed "impairment" The impairment figure for BOC is Rs. 162,905,882,000 which is 4.5 percent of total advances granted. This "impairment" figure includes a category comprising of delayed payments, which are not yet N'PA. The industry norm acceptable for NPAs is 3%.

As stated previously, NPAs of the SOEs are not included here, on the ground that they are covered by Letters of Comfort. As stated previously, these Letters of comfort are no longer valid.

It will be right and proper to call this, a tentative figure in view of the fact that the moratorium on advances granted on a government directive continues to exist, despite the Central Bank calling for an end to it. When the moratorium officially ends in June 2022, there will be a massive cross-over, from performing to non performing with huge consequences.

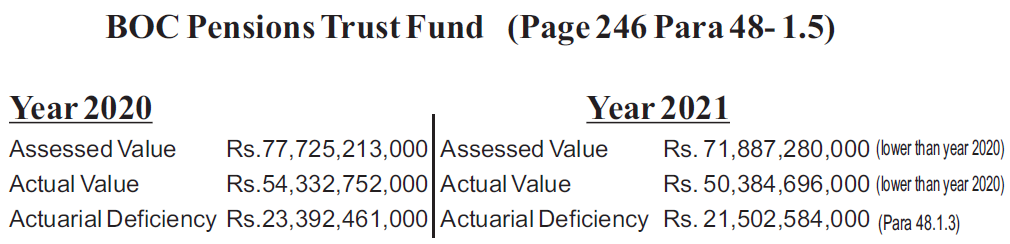

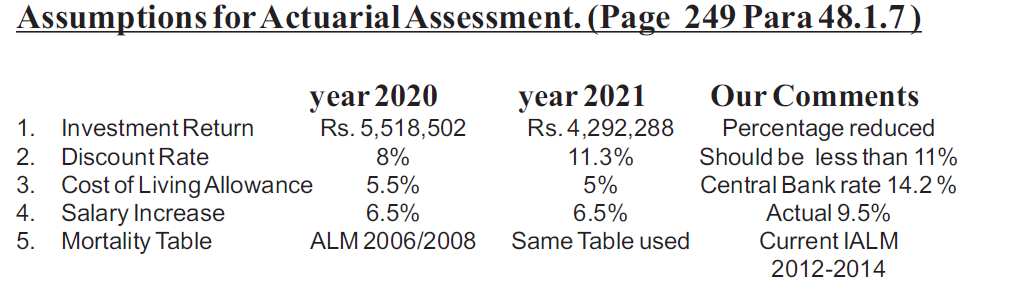

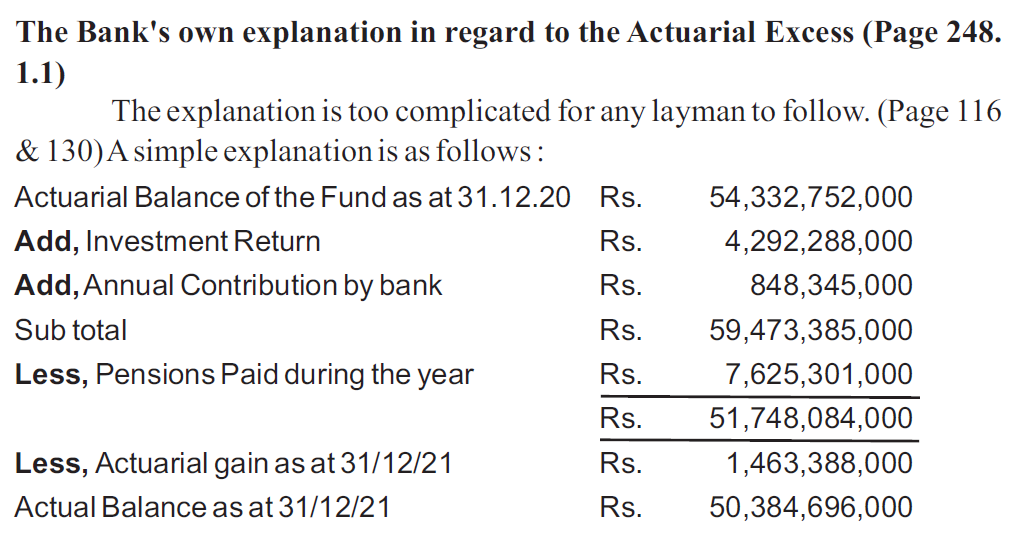

A mere glance at the above figures, prima facie, will suffice for any accountant to see-through the manipulation of these figures. The actuarial deficiency can never get reduced in the absence of a special injection of funds AND in the natural process of added salary increases and the rise in the cost of living allowances, both in large measure, has to increase the deficiency. In this instance the deficiency has magically been reduced by Rs. 1,463,388 in 2021. How come? This is by deliberately, basing the assumptions in the actuarial assessment, on falsely reduced percentages in the computation, as indicated below.

It would be seen that the Bank has unrealistically manipulated these assumptions for 2021, in order to arrive at an excess, to the tune of Rs. 1,463,388,000 and proceeded to transfer a part of this amount to the profit of the year. This is a gross violation of the Trust Fund Law and Regulations in the BOC Pensions Trust Fund and amounts to a Mala Fide act.

(Para 48.1.4) The manner is which this has been done is so complicated that even a senior executive of the Bank will not be able to comprehend the manipulation. But the fact remains that a sum of Rs. 1,463,388,000 has been removed from the Pensions Trust Fund and added to the annual profit of the Bank.

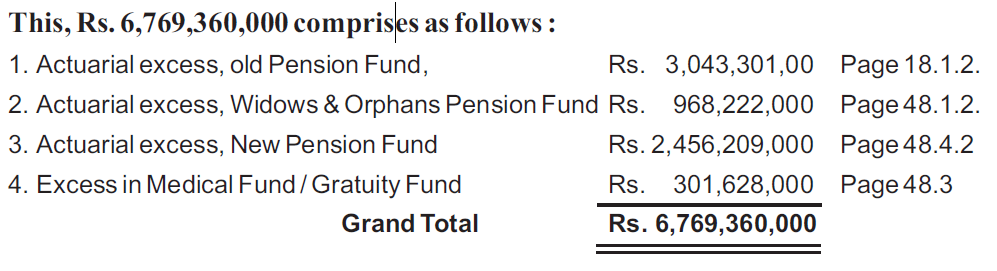

A further examination reveals that not only the Pensions Trust Fund but also the Widows and Orphans Trust Fund and the new entrant Pension Trust Fund have also been, looted on the same basis. The W& O.P Fund has been debited with a sum of Rs. 968,222,000 and the new entrants Pensions Trust Fund has been debited with Rs. 2,456,209,000 on the basis of actuarial gain. A Total of Rs. 6,769,360,000 has been added on to the annual profit for 2021, in this manner.

The actuarial excess has been arrived at by employing unrealistic assumptions in respect of, Discount Rate, Cost of Living Allowance, Salary increase and mortality table. Also, how the return on investmets has been reduced by Rs. 1,226,214,000 has not been explained.

Our re-construction of Fair Value of the Pension Fund using the correct assumptions.

The Statement of Accounts also contains a formula given by the Actuary for any variance that will occur for each of the assumptions by .5 per cent.

Our Experts Panel reconstructed the fair value, on this basis, and they state that at least another Rs. 33 billion should be added to make the final balance, which should be about Rs. 105 billion.

OUR COMMENT :

It appears to \us that, scraping out, the so-called excesses in the Superannuation funds in the manner set out above, has been motivated by feelings of unease of the Corporate Management, in regard to the capital adequacy of the Bank, in terms of Basle III. It is a poor attempt to sustain their claim that the Bank has met with the capital adequacy requirements.

Instead of engaging in these, unlawful interferences in to Trust Funds, managed by different Boards of Trustees, comprising also of elected representatives of the beneficiaries, the Corporate Management should have considered a more honourable way of augmenting their capital base, which is being increasingly threatned at present. The Bank can, invest the entirety or even a part of the Trust Funds in long-term Debentures of the Bank, with perhaps a variable interest schedule, that would benefit both the Bank and the beneficiaries of the Trust Funds, that could ease their current tensions in regard to a possible weakening of their capital base.

Leave a Reply